Depreciation And Cash Flow: How Non-Cash Expenses Shape Real-Life Financial Power

Depreciation And Cash Flow: How Non-Cash Expenses Shape Real-Life Financial Power

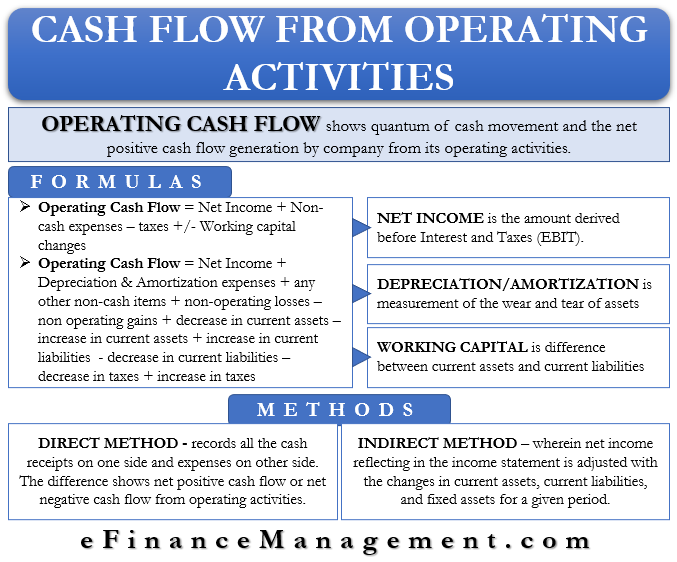

Depreciation isn’t just an accounting entry—it’s a cornerstone of cash flow management that businesses and investors can’t afford to overlook. Linking non-cash charges directly to operational liquidity reveals how companies preserve actual cash, optimize tax planning, and sustain growth. Depreciation, in essence, represents the planned, gradual decline in the value of tangible assets like machinery, buildings, and equipment over their useful lives. Unlike expenses that immediately reduce a company’s bank account—such as wages or raw materials—depreciation is a non-cash deduction.

It reflects wear and tear, obsolescence, or age, not a real outflow of cash. Yet, despite this accounting nuance, depreciation profoundly influences cash flow, particularly operating cash flow. Understanding this relationship is critical for accurate financial analysis and strategic decision-making.

<

As accountant and financial strategist Robert Kiyosaki once stated, “An asset that depreciates doesn’t drain bank accounts—it enables reinvestment.” The timing difference between expenses, profits, and tax liabilities shifts the real cash dynamics. For a business purchasing a $1 million factory machine, annual depreciation on a straight-line basis of 10 years is $100,000. If the company operates in a 25% tax jurisdiction, this depreciation reduces taxable income by the same amount, saving $25,000 in annual taxes—$225,000 over ten years, purely from non-cash allocations.

These savings are real liquidity, not accounting abstraction. Capital assets wear down daily, but depreciation converts that physical erosion into cash flow management leverage. Cash from operations flows more freely, enabling companies to maintain smoother operations through economic cycles and invest in innovation without liquidity crunches.

<

Depreciation schedules dictate timing and magnitude of these non-cash charges, shaping predictable tax savings. Accelerated depreciation methods—such as double-declining balance or bonus depreciation—intensify early tax benefits. For instance, the U.S.

tax code allows 100% bonus depreciation, enabling full cost recovery in the first year for qualifying assets. This strategy drastically accelerates cash flow gains during launch phases, funding rapid scaling. Manufacturers and infrastructure firms use this wisely.

A wind turbine plant might depreciate assets intensively, generating significant upfront tax shields that free capital for new technology or workforce expansion. This reinvestment loop stirs growth—turning depreciation from a mere accounting line item into a strategic lever. Real-world application illustrates the impact: a construction company acquiring $5 million in equipment with a 5-year life and straight-line depreciation records $1 million annual expense.

With a 30% corporate tax rate, this yields $300,000 in annual tax savings. Over five years, this totals $1.5 million—money preserved in the balance sheet, enhancing actual liquidity and creditworthiness. <

Depreciation schedules driven by tax policy—not actual asset usage—may not match actual decline rates. Overestimating useful lives leads to understated early depreciation, inflating reported profits but dazing realistic cash flow planning. Conversely, underestimating can accelerate expenses, straining early earnings.

To navigate this, businesses must align depreciation policies with real-world asset performance. Regular reviews of asset condition and technological readiness form the basis for timely upward or downward revisions. Using data from IoT sensors and predictive maintenance further refines accurate depreciation estimates.

When depreciation mirrors operational reality, companies enhance both financial reporting integrity and cash flow precision. Industry benchmarks matter. Manufacturing and tech sectors typically see higher combined depreciation and cash flow optimization than service-based firms.

Yet even in low-asset industries, depreciation of IT equipment and network infrastructure affects capital allocation and working capital strategies. Ignoring these non-cash flows risks misjudging true liquidity. Investors and analysts increasingly factor depreciation quality into valuation models.

Companies demonstrating stable, realistic depreciation practices signal disciplined financial stewardship—softening cash flow volatility and improving forecast reliability. In essence, depreciation acts as an invisible cash reserve generated through disciplined accounting. It sustains liquidity, reduces tax burdens, and amplifies reinvestment capacity—making it far more than a bookkeeping gesture.

Understanding its flow dynamics enables businesses to harness non-cash charges as strategic financial tools, fostering resilience and growth in a cash-constrained world. Depreciation and cash flow are inextricably linked—non-cash expenses directly sculpt the lifeblood of any operating enterprise, turning planned declines into operational advantages. For companies aiming to thrive, mastering this connection isn’t optional—it’s fundamental.

Related Post

Unveiling the Identity Behind the Spotlight: Wendy Bell, Newsmax Bio Wiki, Age, Height, and Husband Revealed

Q3 2025 marks a pivotal quarter for global markets, economic resilience, and transformative industry shifts—analysis reveals a story of cautious optimism amid evolving dynamics.

Can You Play Battlefield 2042 Offline? Real Possibilities Explained

Mondinion Reveals Undercurrents Shaping Daily Economic Flows: What Daily Updates and Analysis Reveal